How Do HOA CPAs Handle Year-End Closing?

Florida community associations close their books every year, and the final accounting tasks require specific professional expertise. Hoa cpas year-end closing encompasses the work licensed CPAs perform to finalize association financial records at the end of each fiscal year.

Section 720.303 of the Florida Statutes requires associations to complete their annual financial review within ninety days of the fiscal year end. Understanding what CPAs do during year-end closing helps boards prepare and use professional services wisely. Therefore, every board should understand this process before their annual period closes.

Defining Hoa CPAs Year-End Closing

Year-end closing refers to the final accounting procedures that confirm financial records are complete and accurate for the fiscal year just ended. These procedures include finalizing journal entries, reconciling all accounts, and posting accruals. Furthermore, closing also establishes the opening balances for the new fiscal year.

This work differs from routine monthly accounting in both scope and purpose. Monthly accounting maintains current records. Year-end closing confirms the integrity of the entire year’s financial activity. Consequently, this process requires greater attention to detail and more comprehensive verification than any individual month.

What CPAs Review During Year-End Closing

Licensed CPAs examine several critical areas during the year-end closing process. Bank reconciliations for every account must be complete and agree with the general ledger. Furthermore, accounts receivable balances must reflect accurate outstanding assessment totals.

Accounts payable records must show every outstanding vendor obligation as of the fiscal year end. Accrued expenses not yet invoiced must be estimated and recorded so the income statement reflects all costs incurred. Additionally, reserve fund balances must agree with the reserve study schedule and any authorized expenditures during the year.

Adjusting Journal Entries and Accruals

Adjusting journal entries form a core part of hoa cpas year-end closing procedures. These entries correct errors, record missed transactions, and post accruals for revenues earned and expenses not yet recorded. Furthermore, depreciation and amortization adjustments may apply depending on the association’s accounting policies.

Well-documented adjusting entries give boards insight into the quality of their ongoing accounting processes. Boards that receive thorough documentation can identify recurring weaknesses and address them before the next fiscal year. Moreover, recurring adjusting entries for the same items each year signal bookkeeping procedures that need improvement.

Reconciling Reserve Fund Accounts

Reserve fund reconciliation deserves special attention during hoa cpas year-end closing. Each withdrawal from reserve accounts during the year must be traced to an authorized repair or replacement. Furthermore, reserve contributions must match the amounts approved in the annual budget.

Any discrepancy between reserve fund records and actual bank balances must be resolved before year-end statements are finalized. Commingling of reserve and operating funds creates findings that appear in management letters and require immediate corrective action. Therefore, clean reserve fund records at year-end reflect sound governance throughout the year.

Financial Statement Preparation and Review

Once closing procedures are complete, the CPA prepares or reviews the final financial statements. The balance sheet presents the association’s assets, liabilities, and equity as of the last day of the fiscal year. The income statement presents all revenues and expenses for the full twelve-month period. Additionally, the budget comparison report shows how actual results compared to the approved budget for every line item.

These statements represent the official financial record of the association for the year. Boards that review them carefully before distributing to members demonstrate fiduciary responsibility. Similarly, any questions raised should be addressed with the CPA before the reports go to the membership.

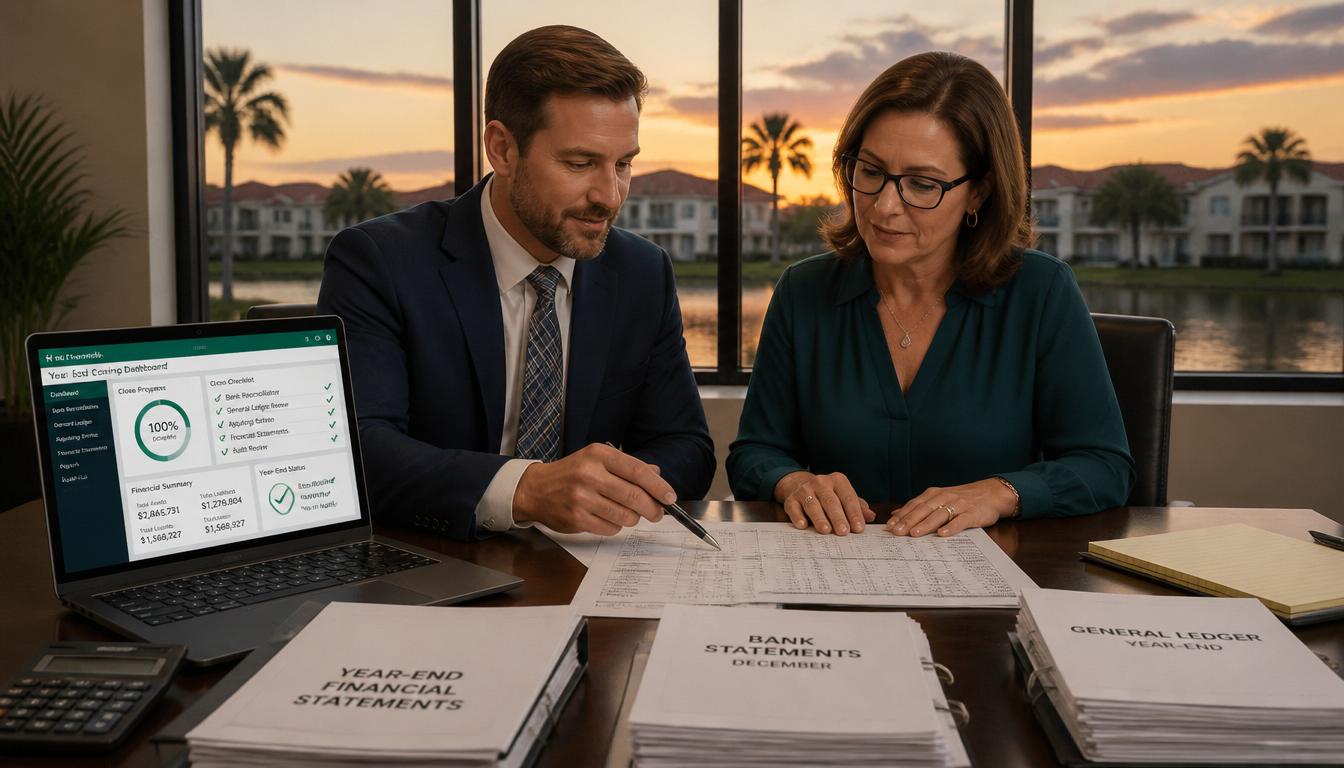

How Technology Supports Year-End Closing

Purpose-built software significantly improves how associations complete hoa cpas year-end closing procedures. Automated bank reconciliation tools reduce the time required to match every account balance against bank statements. Furthermore, accrual tracking features post recurring year-end adjustments automatically, reducing manual entries the CPA must review.

Real-time access to complete, organized financial records allows CPAs to begin their work immediately. Above all, purpose-built software positions the association for a faster, more accurate, and less costly year-end engagement.

Steps for Achieving Goal

- Complete all bank reconciliations for every association account and resolve every outstanding discrepancy before the CPA begins.

- Review accounts receivable balances and identify any amounts that may require an allowance for doubtful collection.

- Confirm all accounts payable obligations are recorded and that accrued expenses are estimated and posted as of year-end.

- Reconcile all reserve fund accounts against authorized expenditures and approved contribution amounts for the year.

- Gather all supporting documents including bank statements, invoices, contracts, and board resolutions for CPA review.

- Review draft financial statements carefully with the CPA before approving and distributing to the membership.

- Adopt purpose-built software that automates bank reconciliations, accrual posting, and financial statement generation for year-end.

Key Takeaways

- Hoa cpas year-end closing encompasses the professional accounting work CPAs perform to finalize association financial records annually.

- Year-end closing confirms the integrity and completeness of the entire fiscal year’s financial activity before any formal review begins.

- Adjusting journal entries correct errors, record missed transactions, and post accruals for the full year.

- Reserve fund reconciliation must trace every withdrawal to an authorized purpose and confirm contribution amounts match the budget.

- Final financial statements represent the official financial record of the association for the fiscal year just ended.

- Purpose-built software reduces CPA engagement time by automating reconciliations, accrual posting, and report generation.

- Boards that prepare clean, organized records for their CPA reduce professional fees and receive faster, more accurate results.

Conclusion

Every Florida community association depends on disciplined hoa cpas year-end closing to produce accurate financial records and fulfill statutory obligations. Boards that support their CPAs with organized, complete records make the year-end process faster, less costly, and more effective.

Strong year-end closing practices do more than satisfy professional standards. Above all, they produce the accurate, complete financial record that every owner deserves and every well-governed association provides. Therefore, associations that invest in year-round accounting discipline and purpose-built technology position themselves for lasting financial confidence.

The information provided on this website is NOT to be considered legal advice. Associations and unit owners should consult with legal counsel for the specific application of the Association’s governing documents and Florida Statutes.

{kind=link}