What Is Florida HOA Fiscal Year Reporting?

Florida community associations operate on a fiscal year schedule that drives every financial obligation they carry. Florida hoa fiscal year reporting governs how associations compile, present, and distribute their financial results at the close of each annual period.

Section 720.303 of the Florida Statutes establishes the financial reporting obligations homeowners associations must fulfill. Understanding these requirements helps boards meet deadlines, satisfy member rights, and demonstrate financial accountability. Therefore, every board should understand what complete fiscal year reporting involves before their annual period closes.

Defining Florida HOA Fiscal Year Reporting

Year-end reporting refers to the complete financial accounting and disclosure process at the close of each annual period. It covers preparing financial statements, completing the required independent review, distributing reports to members, and retaining records. Furthermore, it encompasses reconciling all accounts and establishing opening balances for the new year.

This process differs from monthly financial management in both scope and formality. Monthly reporting tracks operational performance. Year-end reporting produces the definitive financial record that members, auditors, and regulators rely on. Consequently, accuracy and completeness at year-end carry far greater significance than any individual monthly report.

Statutory Deadlines and Timing Requirements

State law requires associations to complete their annual financial review within ninety days of the fiscal year end. This deadline applies whether the association requires a full audit, a review, or a compilation. Therefore, boards must engage their CPA well before the fiscal year ends to ensure the engagement completes on time.

Additionally, associations must distribute the annual budget to members before the start of the new fiscal year. Meeting this timeline requires completing closing procedures promptly so prior year results inform the upcoming budget. Boards that delay year-end closing often miss statutory distribution deadlines as a consequence.

Closing the Books at Fiscal Year End

Closing the books is a critical step in florida hoa fiscal year reporting. It involves reconciling every bank account, confirming all receivables and payables are recorded, and posting all accruals. Furthermore, reserve fund balances must be verified against the reserve study schedule before year-end statements can be finalized.

CPAs who perform the annual review or audit rely on accurate, closed books. Presenting disorganized or unclosed records increases both engagement time and cost. Therefore, completing book closing procedures accurately protects the association from unnecessary professional fees.

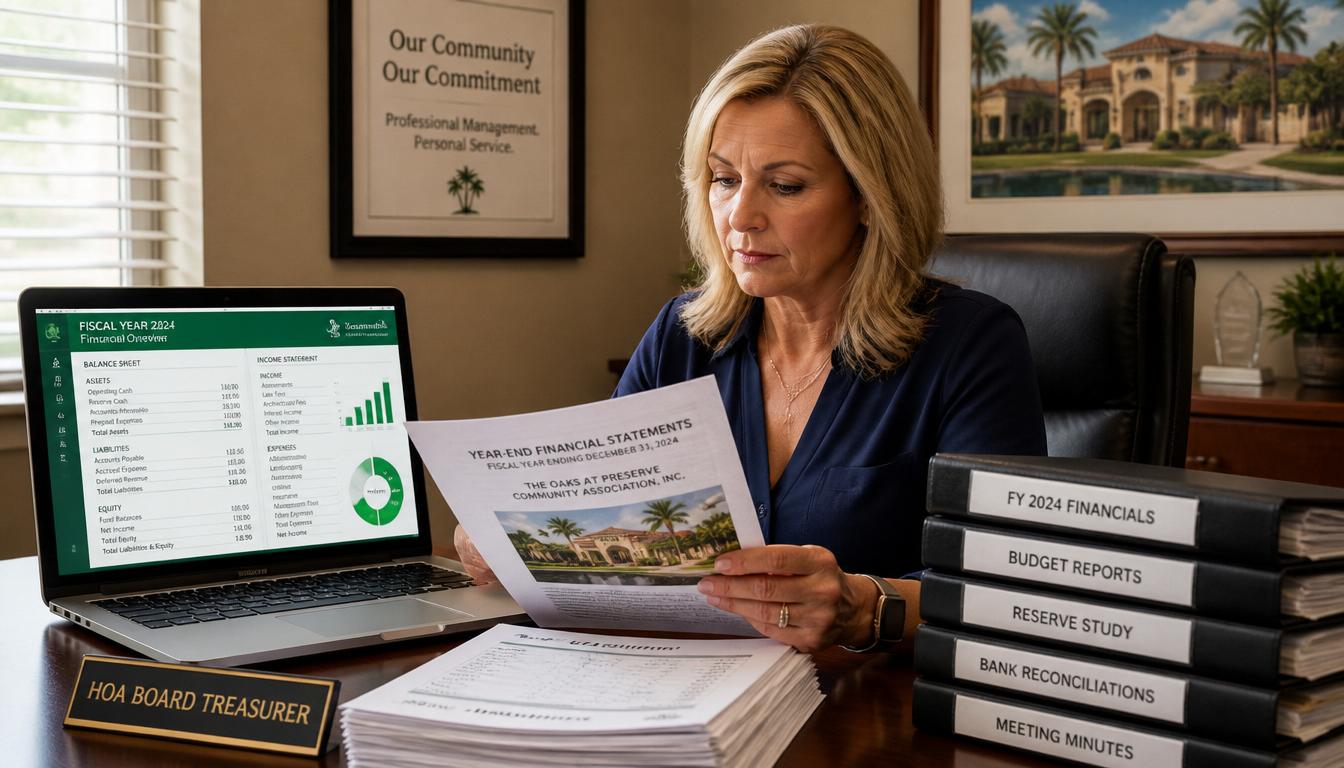

Year-End Financial Statements Required

Accurate florida hoa fiscal year reporting requires a complete set of year-end financial statements. This set includes a balance sheet, a full-year income statement, a budget comparison report, and a reserve fund schedule. Additionally, these statements satisfy the statutory financial reporting obligations boards owe to their membership.

Reserve fund schedules showing each component, its required funding, and its actual balance satisfy statutory reserve disclosure requirements. These disclosures give members visibility into the association’s long-term financial health. Boards that present complete year-end packages demonstrate transparency and professional financial governance.

Member Distribution and Record Retention

Once year-end statements are finalized, the board must fulfill statutory distribution obligations to members. Owners have the right to request and receive financial reports under Florida law. Furthermore, the association must retain all financial records for the periods defined in Chapter 720 and the governing documents.

Organized record-keeping systems significantly simplify both distribution and retention compliance. Associations that maintain digital archives fulfill member inspection requests quickly and accurately. Consequently, well-organized systems reduce the administrative burden of compliance while creating more reliable long-term financial records.

How Technology Supports Fiscal Year Reporting

Purpose-built software significantly improves how associations manage florida hoa fiscal year reporting. Automated year-end reconciliation tools compare every account balance against bank statements simultaneously. Furthermore, integrated financial statement generation produces audit-ready reports directly from closed ledger data without manual compilation.

Secure distribution features deliver year-end financial packages to board members and make reports available to members on demand. Above all, purpose-built software creates the organized, accurate, and complete financial record that every successful year-end process requires.

Steps for Achieving Goal

- Establish a fiscal year closing checklist that covers bank reconciliations, receivable confirmations, payable verification, and reserve schedule review.

- Engage a licensed CPA with community association experience at least sixty days before fiscal year end to schedule the required review.

- Complete all bank reconciliations and resolve every outstanding discrepancy before presenting records to the CPA.

- Verify that reserve fund balances match the current reserve study schedule and document any variances with explanation.

- Prepare year-end financial statements including balance sheet, income statement, budget comparison, and reserve fund schedule.

- Distribute the year-end financial package to the board and make it available to members in compliance with statutory requirements.

- Adopt purpose-built software that automates year-end reconciliation, financial statement generation, and digital record distribution.

Key Takeaways

- Florida hoa fiscal year reporting governs how associations compile, present, and distribute financial results at the close of each annual period.

- Section 720.303 requires associations to complete their annual financial review within ninety days of the fiscal year end.

- Closing the books accurately before engaging a CPA reduces professional fees and speeds the completion of the annual review.

- Year-end financial statements must include a balance sheet, income statement, budget comparison, and reserve fund schedule at minimum.

- Members have statutory rights to request and receive financial reports, making organized year-end records essential.

- Organized record-keeping systems simplify member inspection compliance and create more reliable long-term financial archives.

- Purpose-built software automates year-end reconciliation, report generation, and digital distribution for faster, more accurate reporting.

Conclusion

Strong florida hoa fiscal year reporting closes each annual period with the financial confidence and statutory compliance every Florida community association requires. Boards that approach year-end reporting with discipline protect their communities and demonstrate the professional governance Florida law demands.

Disciplined reporting does more than satisfy legal requirements. Above all, it creates the definitive financial record that guides every decision the association makes in the year ahead. Therefore, associations that invest in year-round financial discipline and purpose-built technology position themselves for stronger outcomes and greater member confidence.

The information provided on this website is NOT to be considered legal advice. Associations and unit owners should consult with legal counsel for the specific application of the Association’s governing documents and Florida Statutes.

{kind=link}